Staffing Payroll Funding: How Recruiters Finance Growth (Including EOR)

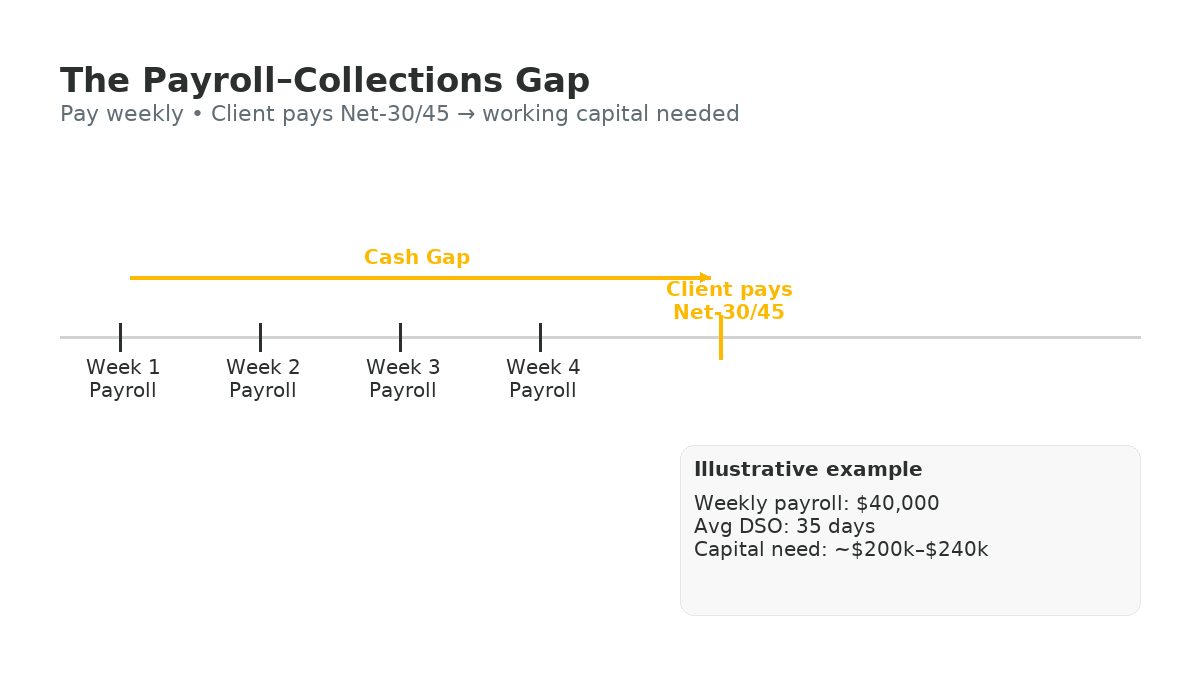

If you run a staffing and recruiting firm, you already know the pain: contractors must be paid weekly, while clients often pay in Net-30/45.

That cash gap is why staffing payroll funding is such a common search—teams need practical ways to finance growth without stalling delivery.

This guide breaks down funding options (factoring, bank lines, MCA, equity) and explains when an Employer of Record (EOR) like BOSS can remove much of the problem by handling payroll, taxes, workers’ comp, and multi-state compliance.

Use the quick chart and table below to compare cost, speed, risk, and capital need—then pick what fits your model.

Staffing Payroll Funding: Simple Comparison

Badges show quick ratings. “Risk retained” = how much employer/payroll/compliance burden stays with you.

| Option | Cost | Speed to Start | Risk Retained by You | Weekly Capital Needed | Notes |

|---|---|---|---|---|---|

| Payroll Funding / Factoring | Medium–High | Fast | High | Medium | Advance against A/R; you still run payroll, taxes, WC/COIs, compliance. |

| Bank Line of Credit (LOC) | Low | Medium | High | Medium | Cheapest when approved; covenants/reporting; you still fund weekly payroll (via the line). |

| Merchant Cash Advance (MCA) | Very High | Fast | High | Low* | Quick cash but aggressive repayment can strain cash flow. *Low upfront capital, high daily pulls. |

| Equity / Investor Capital | Varies* | Slow | Medium | N/A | Dilutes ownership; good for strategic growth, not for next week’s payroll. *Depends on deal. |

| EOR (BOSS) | Low–Medium | Fast | Low | Low | BOSS is the Employer of Record: payroll, taxes, WC/COIs, multi-state compliance handled; you recruit and manage the client. |

Illustrative only; actual pricing/terms vary by volume, credit, and program.

Why Staffing Payroll Funding Exists (and the Simple Math)

- Cash conversion reality: You pay Friday; collections land 30–45 days later.

- Growth penalty: Each new contractor adds payroll before collections arrive.

- Risk: One slow-pay client can choke hiring, delivery, and margins.

Quick model: If weekly payroll is $40,000 and average DSO is 35 days, you may need roughly $200K–$240K of accessible working capital to grow comfortably.

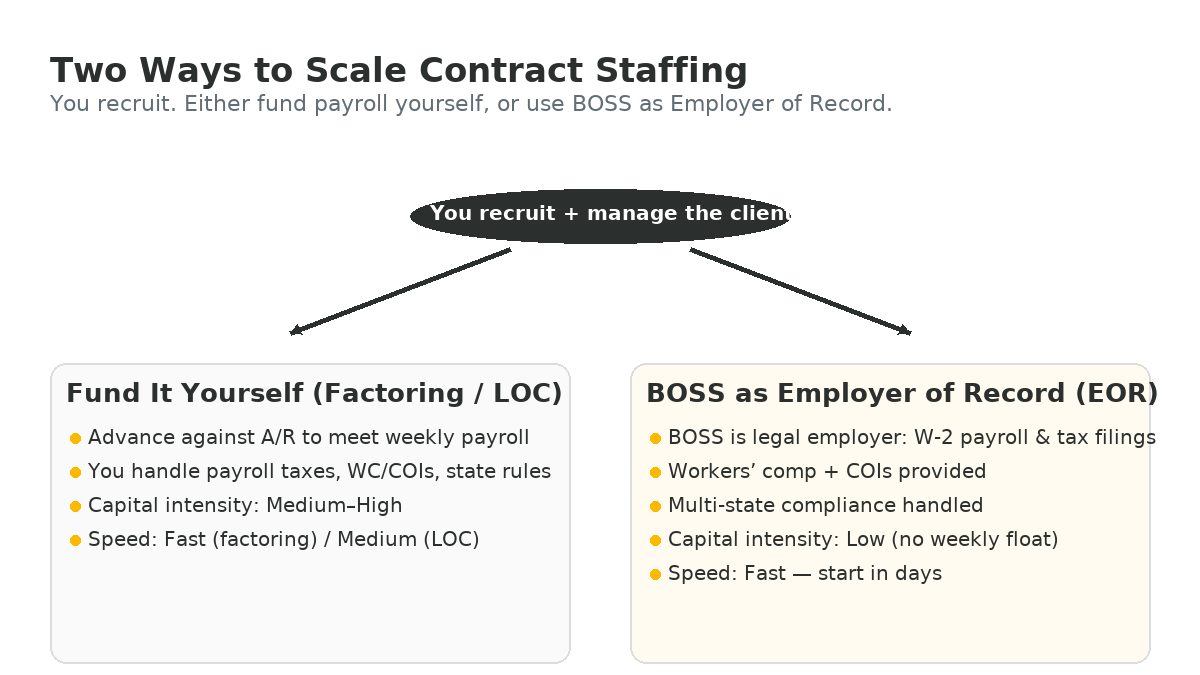

Staffing Payroll Funding Options (and When EOR Wins)

| Option | What It Is | Pros | Cons | Best For |

|---|---|---|---|---|

| Payroll Funding / Factoring | Advance against approved A/R; fund in 24–48 hours once set up. | Fast, scales with receivables; lighter covenants than banks. | Fee/discount cost; UCC/notice of assignment; you still run payroll, taxes, WC/COIs, compliance. | Early growth or when bank credit is limited. |

| Bank Line of Credit (LOC) | A/R-based revolving line, typically lower cost than factoring. | Lower cost of capital; client relationship remains direct. | Harder underwriting; covenants/reporting; you still own payroll & compliance. | Established firms with clean financials and predictable A/R. |

| MCA | Advance repaid via daily/weekly withdrawals or card volume. | Very fast. | High effective cost; aggressive repayment; misaligned with net terms. | Emergency bridge only (use with caution). |

| Equity / Investor Capital | Sell a slice of ownership for growth capital. | No debt service; potential strategic help. | Dilution and longer timelines; not a near-term payroll fix. | Large strategic moves (new markets, M&A). |

| EOR (BOSS) | Employer of Record for staffing—BOSS becomes legal employer, runs W-2 payroll, taxes/filings, benefits, WC/COIs, multi-state compliance. | Capital-light scaling; faster multistate; risk offload (tax, wage/hour, WC); you keep client & recruiting. | Service fees; process alignment needed; EOR runs the employment layer. | Adding contract/temp fast, multi-state, less capital and employer risk. |

Option 1: Payroll Funding (Factoring)

What it is: You sell or pledge invoices and receive an advance; the funder collects later.

Typical pricing is a fee or discount (varies by credit/volume). You still manage weekly payroll, payroll tax deposits, certificates of insurance (COIs), and classification.

Try it when: speed matters and bank credit is tight. Revisit a bank LOC as you mature, or evaluate EOR to shrink the capital need.

Option 2: Bank Line of Credit

What it is: A revolving A/R-based facility. Usually cheapest capital if you qualify, but requires clean financials and covenants.

Try it when: you can pass underwriting and want to keep employment ops in-house.

Option 3: MCA (Use Sparingly)

MCAs fund fast but the repayment cadence can strain cash flow in staffing. Treat as a true last resort.

Option 4: Equity

Great for strategic expansion, not a solve for next Friday’s payroll. Combine with LOC or EOR depending on your model.

Option 5: EOR (BOSS) — The Capital-Light Alternative

With BOSS as your EOR, we become the employer of record for your placed contractors.

We handle W-2 payroll, tax filings, benefits admin, workers’ comp & COIs, and multi-state rules (OT, sick leave, notices).

You keep the brand, client relationship, and recruiting engine—without floating weekly payroll in new states.

- Capital light: fund fewer dollars (or none) between pay day and DSO.

- Multi-state speed: place talent in any state without creating entities.

- Risk transfer: employer risks and coverage sit with the EOR program.

Which Path Should You Pick?

- Need cash tomorrow & can’t qualify for a bank line? Start with factoring; revisit LOC or EOR as you scale.

- Want lowest cost and own payroll ops? LOC + strong internal compliance.

- Want to add contract/temp fast across states with less capital? Go EOR (BOSS).

Next Steps & Resources

• See how we stack up: compare EOR providers.

• Bonus resource: free AI playbook for recruiters — The Smart Recruiter’s AI Handbook.